There is an architect at your firm making $50 an hour. But the client gets billed $150 for that same hour. Where does that $100 gap go? And what happens to your firm financially if you get that number wrong? That is what this post is about. From staff work plans to the overhead rate formula, from utilization and break-even rate to the net multiplier and profit, this is how architecture firm finances actually work behind the scenes.

This podcast is also available on YouTube, Spotify, and Apple Podcasts

What Is a Staff Work Plan?

If you work at an architecture firm right now, there is a document floating around most architecture firms that you have probably never seen.

It is called a staff work plan, and it is one of the most important documents in the entire practice.

A staff work plan is an internal management tool. It is not something your clients ever see. It is not in the contract, the specs, or the project manual. It stays inside the firm.

Think of it like the budget you would make before a road trip. Before you leave the driveway, you need to know how much gas costs, where you are stopping for food, and what the hotel runs. You do not just get in the car with your credit card and hope for the best.

A staff work plan works the same way, except instead of gas and hotels, you are budgeting people’s time and salaries.

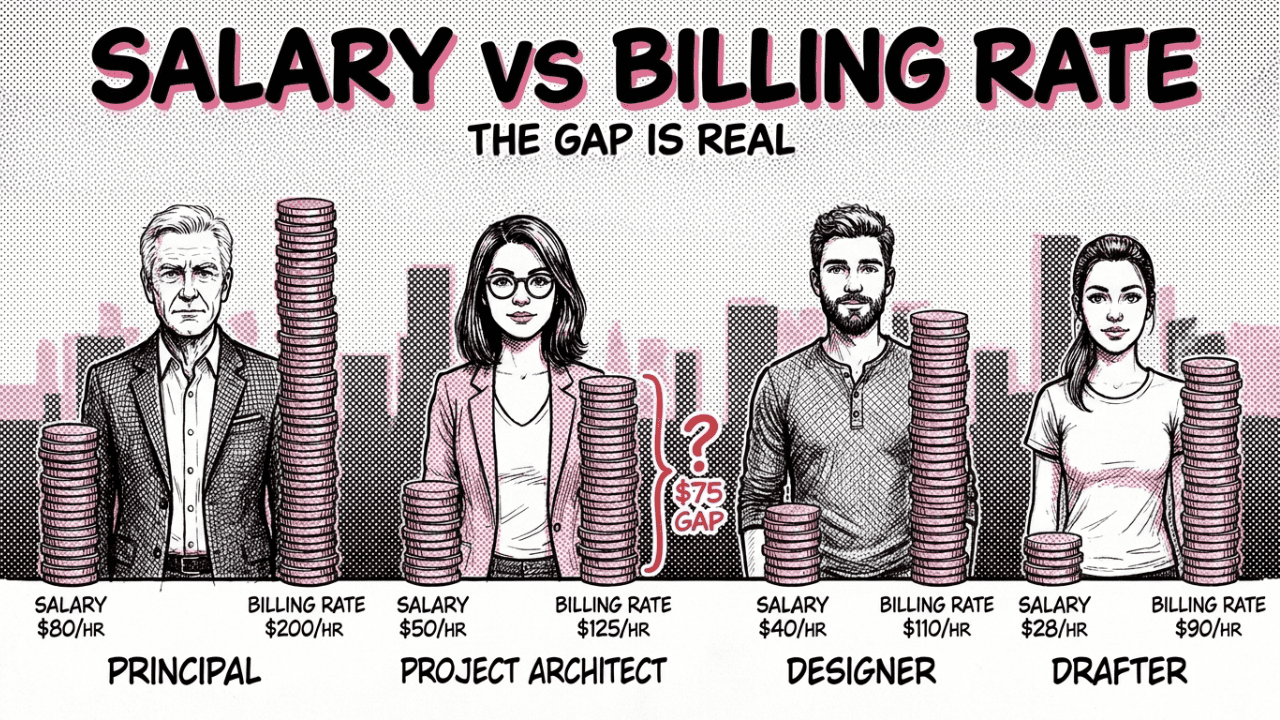

It lists out every person on the project team, their role (principal, project architect, designer, drafter), what each person gets paid per hour, and what each person gets billed to the client per hour.

And those two numbers are very different.

Take someone like Kelly. Kelly is a project architect. She makes $50 an hour. That is her salary, that is what shows up in her paycheck.

But when Kelly works on a project, the client does not get invoiced at $50. The client gets invoiced at $150 an hour for Kelly’s time.

It works like that for everyone at the firm. A drafter might make $28 an hour but get billed at $90. A principal might take home $80 an hour but their billing rate is $200. If you want to see how architect fee structures fit into this picture, that post covers the different ways firms charge for their services.

The specific numbers are not what matters here. What matters is understanding that there is always a gap between what staff earns and what the firm charges the client for that person’s time.

The rest of this post is about understanding where that gap goes and why it has to exist.

Direct Labor vs Indirect Labor

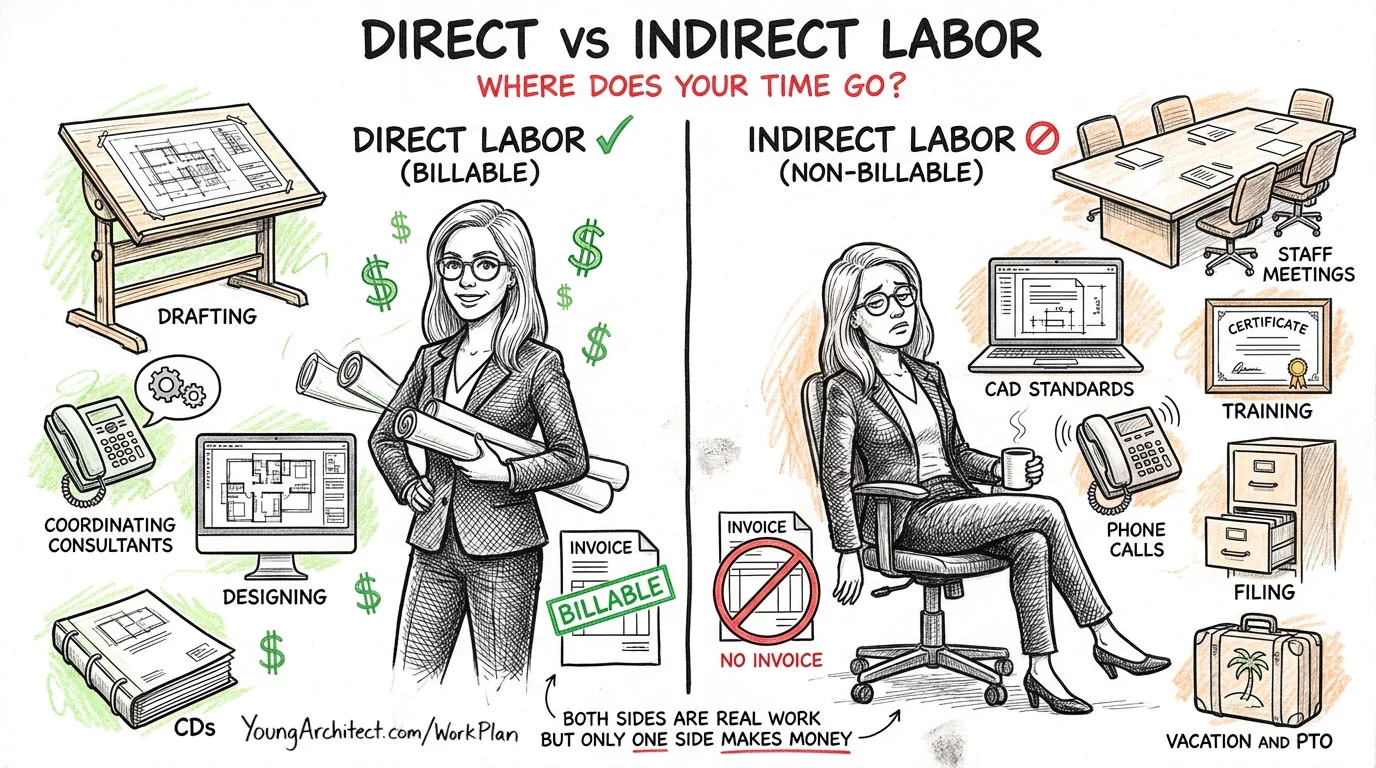

Not every hour someone spends at the office is billable to a client. Understanding that distinction is foundational to everything else.

Direct labor is time spent working directly on a project that you can bill to a client:

- Designing

- Drafting

- Coordinating consultants

- Producing construction documents

If it is tied to a specific project and you can put it on an invoice, that is direct labor.

Indirect labor is everything else:

- The Monday morning staff meeting

- Updating the firm’s CAD standards

- Training (Revit courses, management coaching)

- Answering the phone for a potential new client

- Organizing shared drives and filing

- Vacation time and paid time off

All of that is real work. It is necessary. And your people need to be paid for it. But there is no project to charge it to.

The cost of all that indirect time has to come from somewhere. And that somewhere is baked into the gap between salary and billing rate.

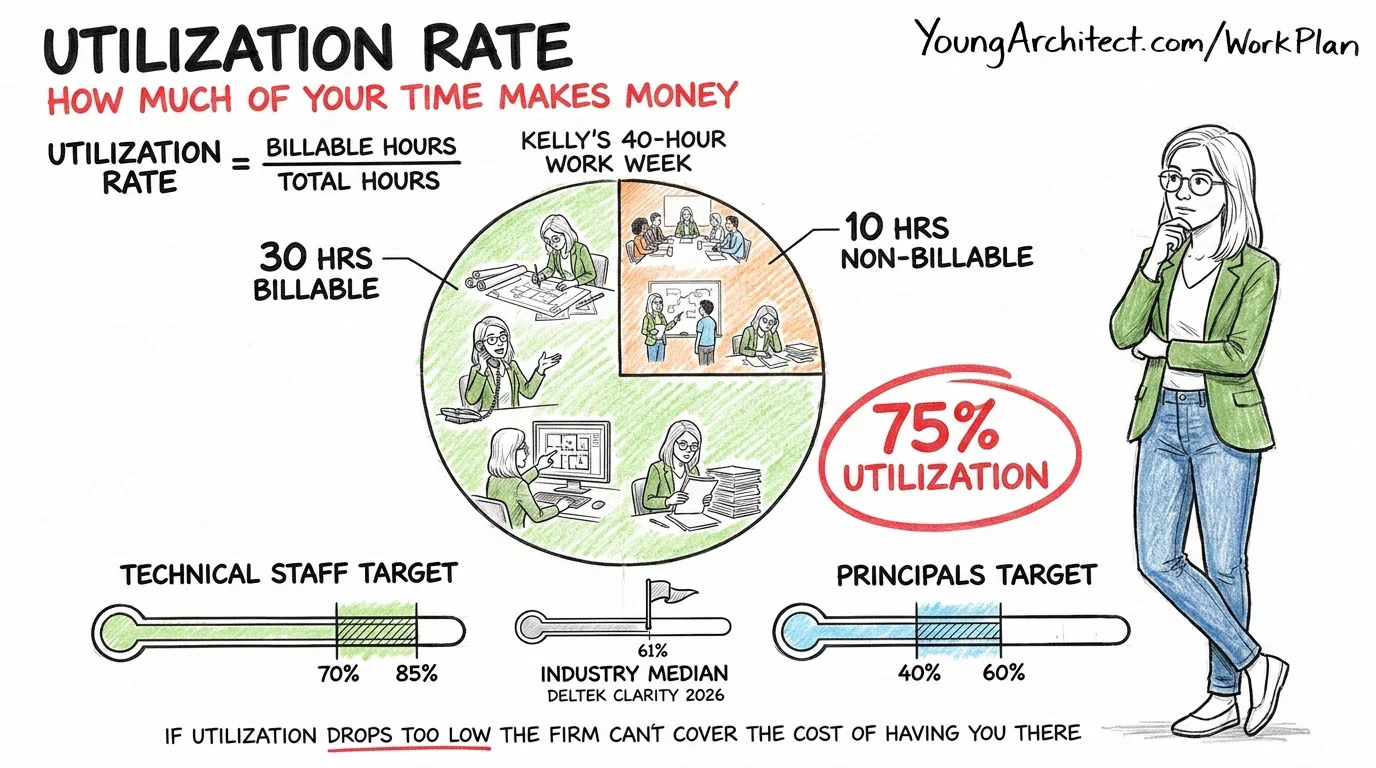

Utilization Rate: How Much Time Is Actually Billable?

If not every hour is billable, then how much of your staff’s time is actually generating revenue?

That is what the utilization rate measures.

Utilization rate = billable hours / total hours

Back to Kelly. She works 40 hours a week. But not every one of those hours is directly billable.

There is a staff meeting that lasts an hour. A couple of phone calls that are not tied to a current project. Some time mentoring a new hire. An hour updating the office BIM template. A few internal emails about scheduling and PTO. All important, but none of it is going on a client invoice.

Out of her 40 hours, maybe 30 are directly billable. That gives Kelly a utilization rate of 75%.

That means 25% of her time at the office is not generating revenue. And the firm still has to pay her for all 40 hours.

What is a good utilization rate?

- Technical staff (designers, project architects, drafters): 70 to 85%

- Principals: 40 to 60% (they spend significant time running the business, chasing new projects, and meeting prospective clients)

- Industry median (firm-wide): about 61% according to the latest Deltek Clarity data

One important distinction: that 61% median is a firm-wide average that includes everyone, from admin staff to principals. Individual technical staff targets are higher than the firm-wide number. Keep that distinction clear: individual staff targets and firm-wide averages are different numbers and get used differently.

If utilization drops too low across the firm, you have a problem. You are paying people to be there, but you are not generating enough revenue to cover the cost.

For a deeper look at how firms measure financial health, Deltek’s overview of key financial performance indicators for architecture firms covers utilization and several other metrics worth knowing.

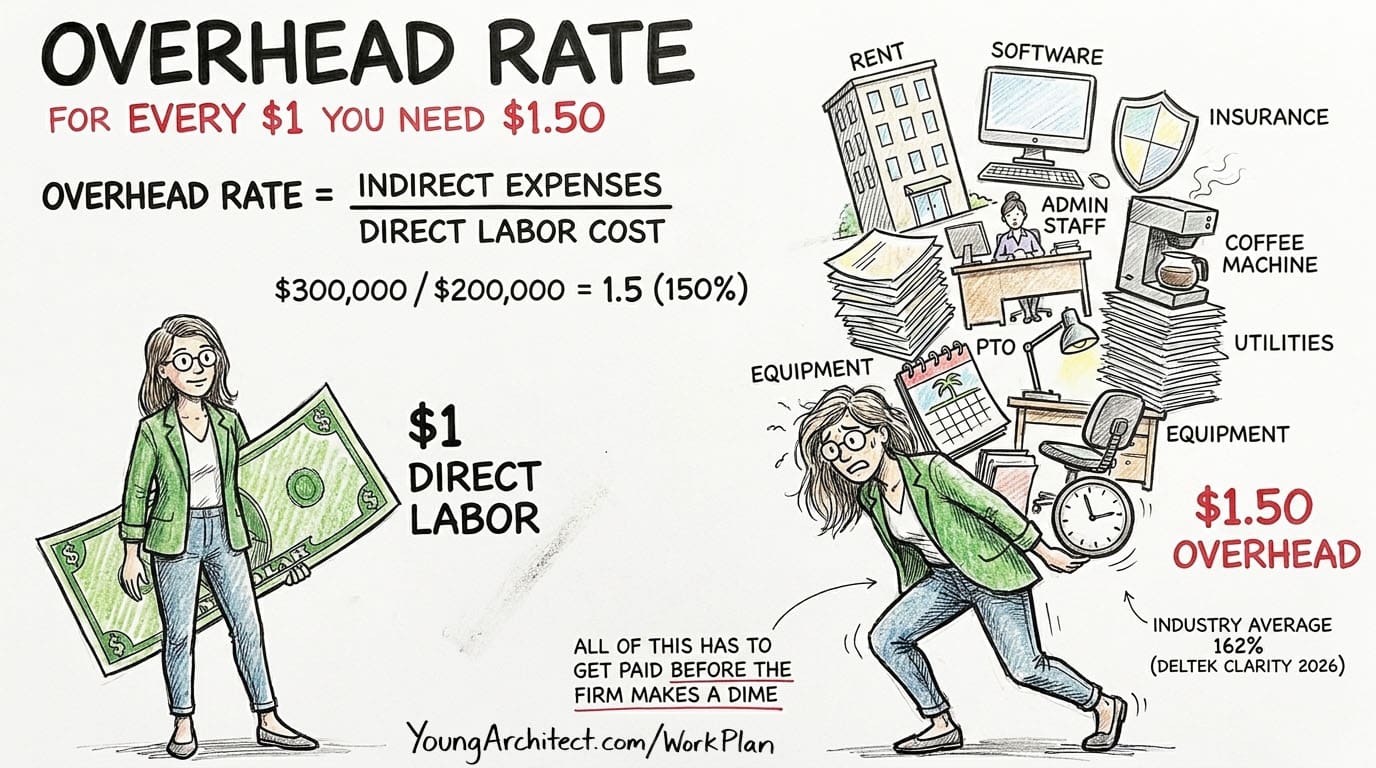

Overhead Rate Formula: The Cost of Keeping the Lights On

Everything it takes to run your firm that is not directly tied to a project? That is your overhead. And it adds up fast.

Think of it like running your household. You cannot just look at your paycheck and think all of that money is yours to spend however you want. Rent, utilities, insurance, groceries, and your car payment all get covered first, or things fall apart. Running a firm works the same way.

What counts as overhead:

- Office rent

- Business insurance

- Software licenses (AutoCAD, Revit)

- Admin staff salaries (front desk, HR, accounting)

- Utilities and office equipment

- All that indirect labor (meetings, training, PTO)

None of that gets billed to a specific client. But all of it has to get paid for.

The formula:

Overhead rate = indirect expenses / direct labor cost

Here is an example. Your firm’s total indirect expenses come out to $300,000 a year. The total direct labor cost (salaries paid for time spent directly on projects) is $200,000 a year.

Your overhead rate is $300,000 / $200,000 = 1.5, or 150%.

The latest Deltek Clarity study puts the industry average for architecture firms at about 162%. So real-world overhead is often even higher than the example we are using here.

What does 150% mean in plain English?

For every dollar you spend on staff doing project work, you need another dollar and fifty cents just to keep the business running. Desks, computers, software, insurance, the person at the front desk. All of it.

If you do not account for that overhead rate in what you charge your clients, eventually the lights go off.

This is exactly the kind of financial thinking we break down in our PcM 101 course, with case studies and practice problems that let you work through the math yourself. It is part of the ARE 101 Membership, which gives you access to every course for one monthly price.

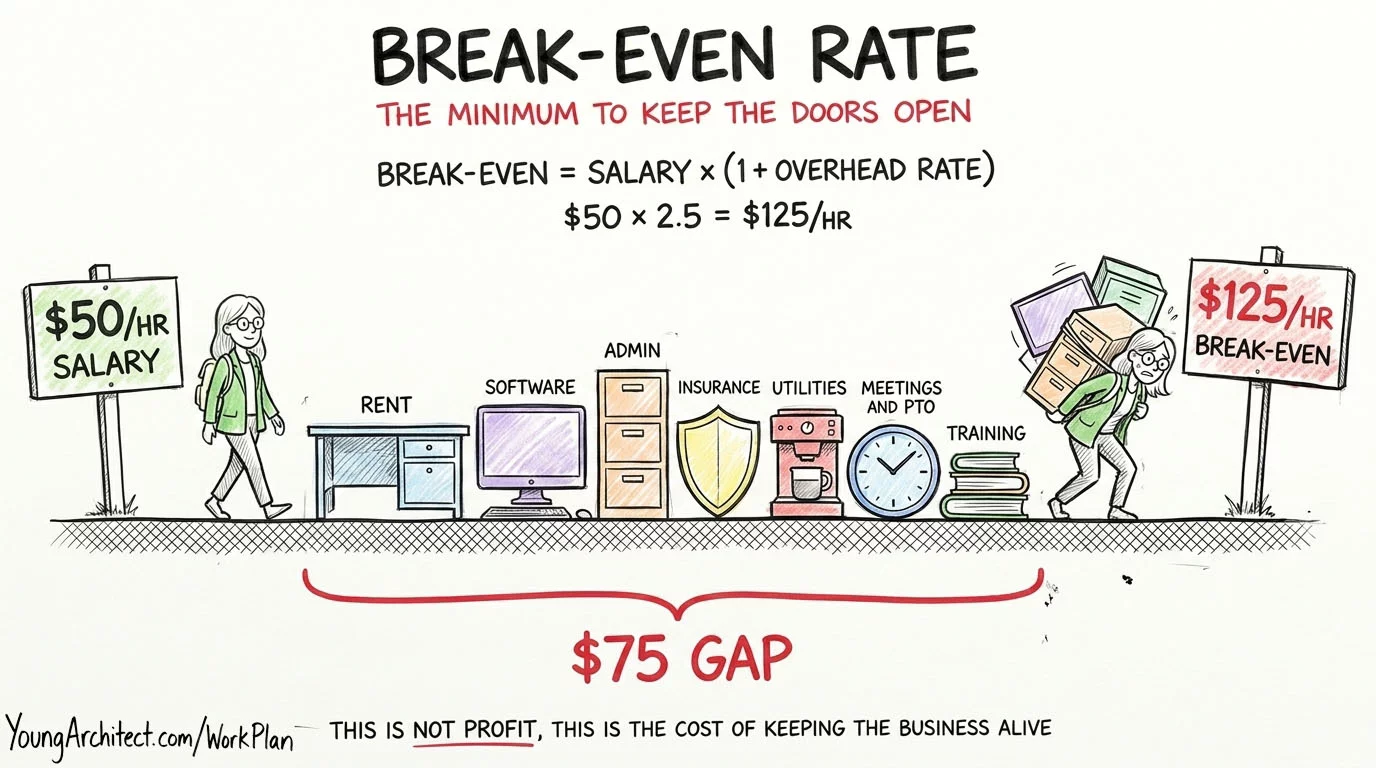

Break-Even Rate: The Minimum You Need to Charge

Now you know what overhead costs. The next question is: what do you need to charge per hour just to not lose money?

That is the break-even rate. The minimum you need to bill per hour to cover your costs. Not profit. Not growth. Just survival.

Think of it like treading water. You are not drowning, which is great. But you are not going anywhere either. You need to get above that line to actually move forward.

The formula:

Break-even rate = salary x (1 + overhead rate)

Back to Kelly. She makes $50 an hour. The firm’s overhead rate is 1.5.

$50 x 2.5 = $125 per hour.

That is the break-even rate. Even though Kelly takes home $50 an hour, the firm needs to bill at least $125 per hour for her time just to cover expenses. If the firm bills anything less than $125 for Kelly’s time, they are losing money on every single hour she works.

Now, remember the hook from the top of this post. Kelly makes $50 and the client gets billed $150.

That $100 gap between salary and billing rate? The first $75 of it goes to overhead. That is the break-even cost. The remaining $25 is where profit comes from.

The break-even rate tells you the minimum you need to survive. But nobody starts a business just to break even.

The next section shows exactly how that $150 billing rate gets set.

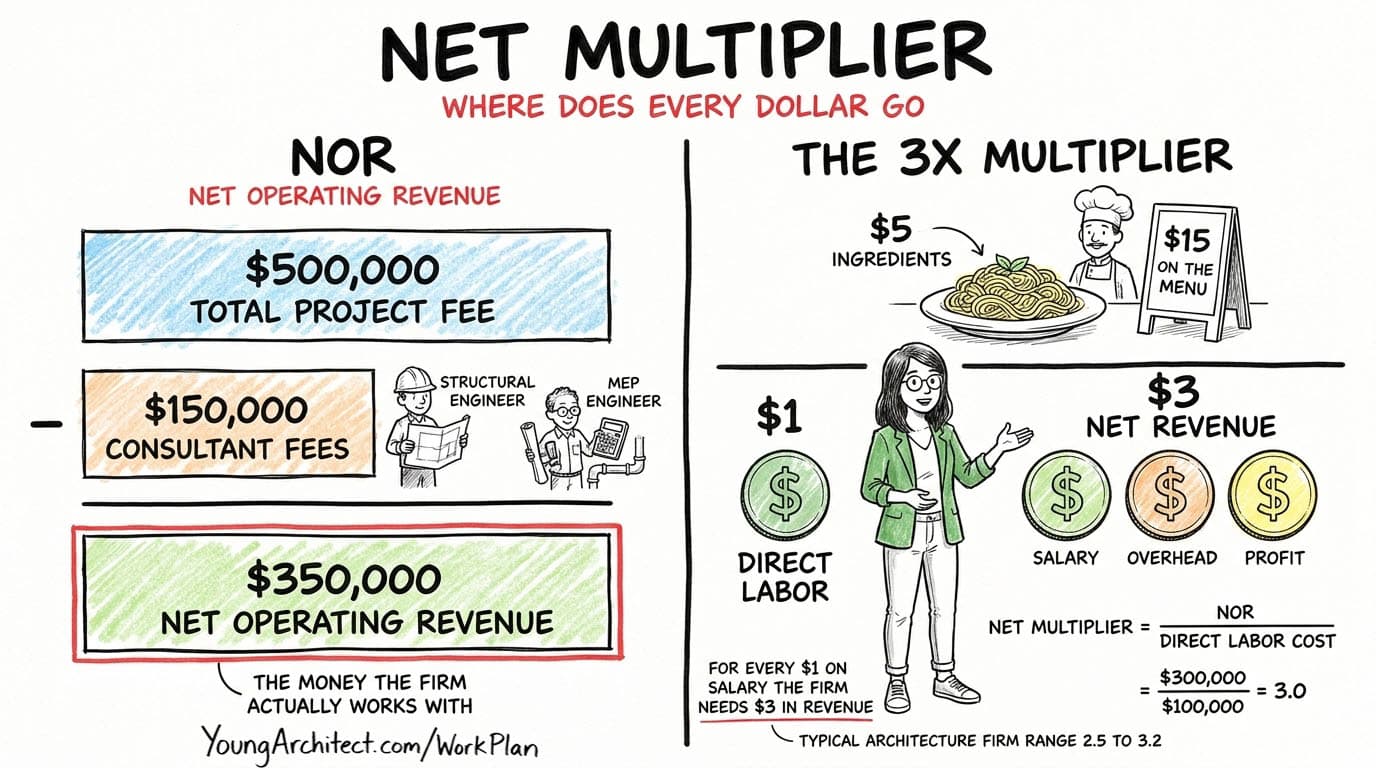

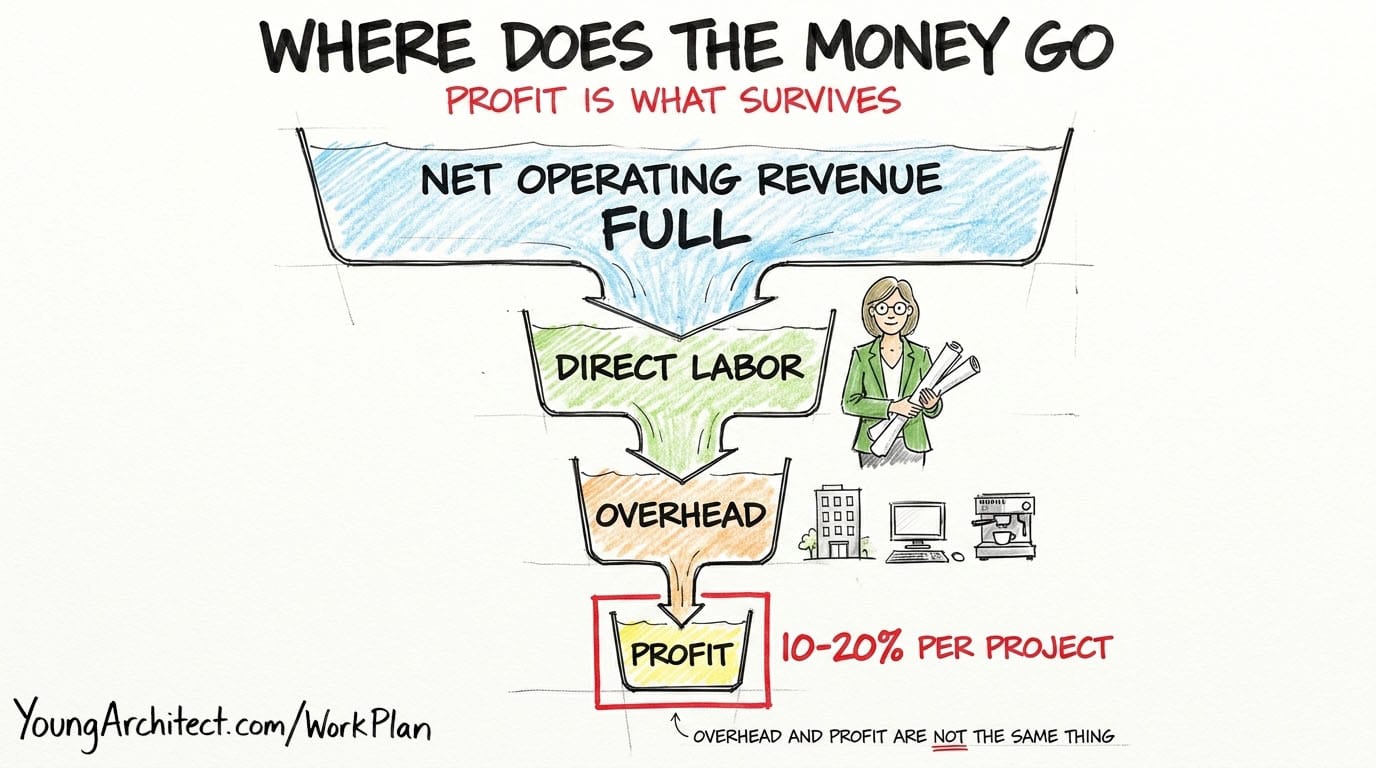

Net Multiplier and Net Operating Revenue

Before we get to the billing rate formula, there is one definition you need first.

Net Operating Revenue (NOR) is the money the firm actually has to work with after subtracting consultant fees, reimbursable expenses, and direct project costs that just pass through the firm.

If a client pays your firm $500,000 for a project, but $150,000 of that goes straight to the structural engineer and the MEP consultant, your net operating revenue is $350,000. That $150,000 was never really yours. It just passed through your bank account on its way to someone else.

The net multiplier formula:

Net multiplier = net operating revenue / direct labor cost

For a typical architecture firm, the net multiplier falls somewhere between 2.5 and 3.2.

Think of it like a restaurant. A plate of pasta might cost $5 in ingredients, but the restaurant charges $15 because they need to pay the chef, the server, the rent, and the dishwasher. That $15 is not a ripoff. It is what it costs to run the business. Architecture firms work the same way. For every $1 the firm spends on staff salary, it needs to bring in $3 in net revenue to cover salary, overhead, and profit.

And here is where it all connects back to Kelly.

If the firm’s target net multiplier is 3.0, then Kelly’s target billing rate is her salary multiplied by that number.

$50 x 3.0 = $150 per hour.

That is the same $150 from the hook. Now you know exactly where it comes from. The break-even rate ($125) covers costs. The net multiplier ($150) covers costs and leaves room for profit.

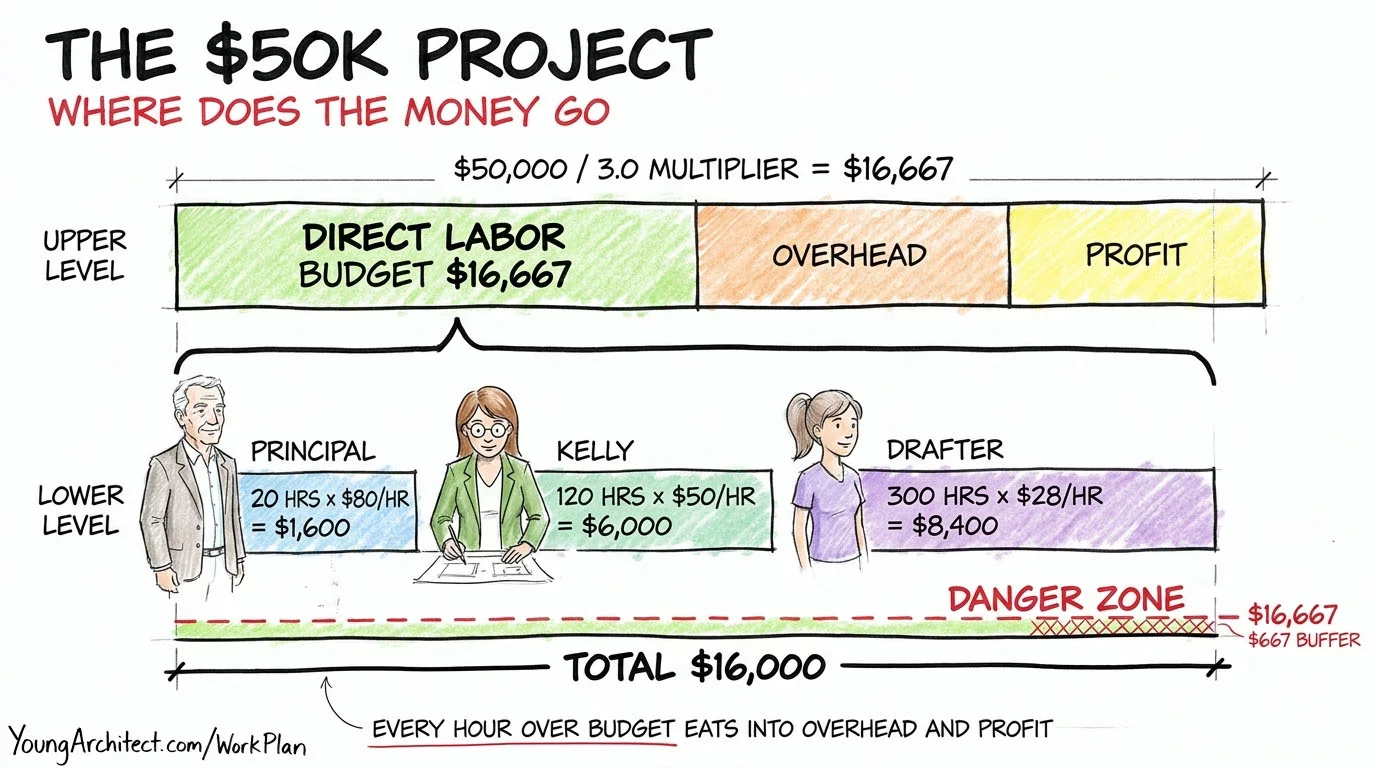

Staffing a Project: The $50K Example

A client reaches out about a new project. They have a budget of $50,000 for architectural services.

But here is what a lot of people do not realize. Just because you have a $50K budget does not mean you have $50,000 to throw at your staff.

Your firm’s net multiplier is 3.0. To find out how much you can actually spend on staff salaries, divide that fee by 3.

$50,000 / 3 = $16,667

That is your direct labor budget. The total amount you can afford to spend on staff salaries for this project. The other two-thirds of that fee goes to overhead and profit.

Now you need to staff the project within that budget.

Three people on this one:

- Principal at $80/hr: 20 hours = $1,600

- Kelly (project architect) at $50/hr: 120 hours = $6,000

- Drafter at $28/hr: 300 hours = $8,400

Total staff cost: $16,000. Just under the $16,667 budget. On track, with a small buffer.

But here is the critical takeaway.

If anyone on that team goes over their estimated hours, the firm starts eating into overhead and profit.

The principal takes on a few extra meetings. Kelly has to redo drawings because of a scope change. The drafter hits a snag and puts in extra time. Suddenly you are over $16,667, and the firm is losing money on this project even though they have a signed contract and a decent fee.

Even on a fixed-fee project where the client is not paying by the hour, the firm still tracks hours internally against that direct labor budget. That is how you know whether you are on track or whether you are bleeding money.

This connects to how construction cost estimates evolve across project phases, and why understanding hard costs vs soft costs helps you see where the architectural fee fits in the bigger financial picture.

This is exactly the kind of thinking NCARB’s objectives are pointing toward when they reference project financial management. Can you look at a fee, apply a multiplier, and figure out how to staff the project without going over budget?

Overhead vs Profit: They’re Not the Same Thing

There is a distinction that gets mixed up constantly.

Overhead is the cost of doing business: rent, software, insurance, admin. All those indirect costs we have been talking about.

Profit is what is left after you have paid for both direct labor and overhead.

Profit = net operating revenue – direct labor – overhead

For a typical architecture firm, the target is somewhere between 10 and 20% profit on each project.

Here is something to keep in mind. A firm can be profitable overall while losing money on individual projects. And the reverse is true too. You can have a project that looks profitable on paper, but if your other projects are dragging you down, the firm is still struggling.

That is exactly why staff work plans matter. They help you catch the losing projects before they drag down the whole practice.

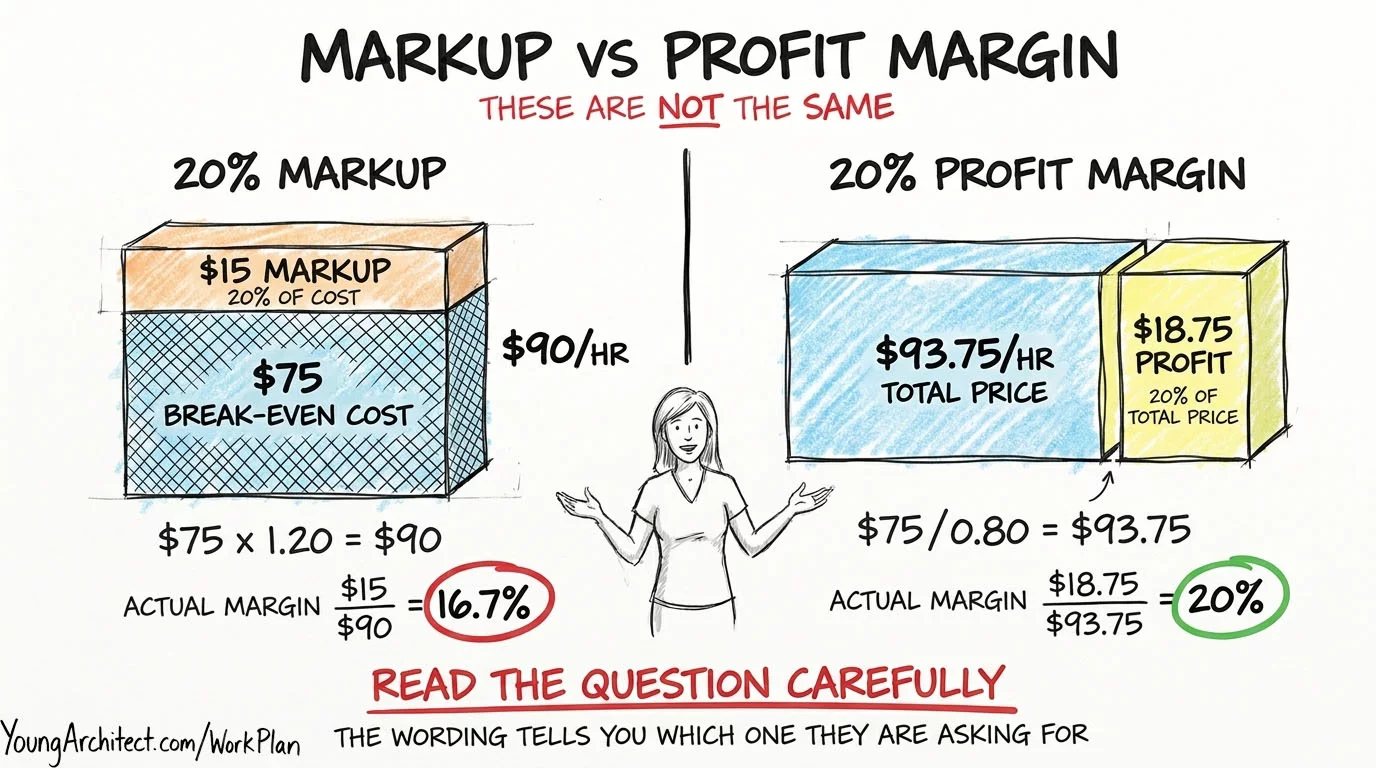

Markup vs Margin: They’re Not the Same Thing

This is the distinction that catches people off guard, so take your time with it.

Here is the setup. You are given an overhead rate of 1.5, a staff salary of $30 an hour, and a target profit of 20%.

What is the billing rate?

Step one. Calculate the break-even rate.

$30 x (1 + 1.5) = $30 x 2.5 = $75 per hour

Step two. This is where it gets tricky.

Your instinct might be to take $75 and multiply by 1.20 to add 20% on top. That gives you $90 per hour.

But that is a 20% markup on cost. It is not a 20% profit margin.

Markup means you are adding 20% on top of your cost. $75 + 20% of $75 = $90. But the profit in that $90 is $15. And $15 out of $90 is only 16.7%. Not 20%.

Profit margin means profit is 20% of the total billing rate. To get that, take $75 and divide by 0.80. That gives you $93.75. The profit is $18.75, and $18.75 out of $93.75 is exactly 20%.

The billing rate changes depending on whether the scenario calls for markup or margin. And those two words look really similar when you are reading quickly.

Markup and margin are not the same thing. If you remember one thing from this section, remember that. The wording matters because the math changes.

How This Shows Up on the PcM and PjM Exams

Everything we just covered falls primarily under PcM and PjM.

NCARB’s published objectives for those divisions specifically reference financial management, resource allocation, and project budgeting, which is exactly what this post walks through.

In PcM, the objectives point toward evaluating the financial health of your practice. Understanding what it costs to resource your firm, what your overhead rate looks like, and whether your billing rates are sustainable.

In PjM, the objectives point toward building a work plan for a specific project. Allocating staff, estimating hours, and tracking whether you are on budget.

NCARB’s objectives expect you to understand how these concepts connect. The financial relationships between overhead, utilization, billing rates, and profit are not isolated formulas. They work together, and the three pro practice exams each approach them from a different angle.

For the official breakdown of what PjM covers, NCARB’s published objectives for PjM list the specific competency areas.

If this is the kind of content that is clicking for you, come study with us.

The ARE Boot Camp is a coaching program that gives you a structured study plan, weekly accountability, and a community of candidates working through the exams alongside you. It is more than study materials. It is the structure that keeps you actually studying.

If you prefer to go self-paced, the ARE 101 Membership gives you access to every course we offer for one low monthly price, cancel anytime. For this topic specifically, PcM 101 covers financial concepts with case studies and practice problems, PjM 101 covers project work planning and resource allocation, and AIA Contracts 101 covers the contract structures that drive how fees and billing work.

Now go pass this exam.

Frequently Asked Questions

What is overhead rate in architecture?

The overhead rate is the ratio of a firm’s indirect expenses to its direct labor cost. It measures how much it costs to run the business for every dollar spent on billable project work. For architecture firms, a typical overhead rate falls between 150% and 175%, meaning the firm spends $1.50 to $1.75 on overhead for every $1.00 of direct labor. The formula is indirect expenses divided by direct labor cost.

What is the difference between direct labor and indirect labor?

Direct labor is time spent working on a specific project that can be billed to a client, like designing, drafting, or producing construction documents. Indirect labor is everything else: staff meetings, training, vacation time, marketing, and administrative tasks. Both are real work that staff need to be paid for, but only direct labor generates revenue. The cost of indirect labor gets absorbed into the firm’s overhead rate.

How do you calculate the break-even rate for an architecture firm?

The break-even rate formula is salary multiplied by one plus the overhead rate. If an architect makes $50 per hour and the firm’s overhead rate is 1.5, the break-even rate is $50 times 2.5, which equals $125 per hour. That means the firm must bill at least $125 per hour for that person’s time just to cover costs before any profit.

What is the difference between markup and profit margin?

Markup adds a percentage on top of your cost. Profit margin is the percentage of total revenue that is profit. A 20% markup on a $75 break-even rate gives $90, but the actual profit margin is only 16.7% ($15 out of $90). A 20% profit margin requires dividing $75 by 0.80, giving $93.75, where $18.75 out of $93.75 is exactly 20%. The formula changes depending on which one is being calculated.

What is a good utilization rate for architects?

For technical staff like project architects and drafters, most firms target a utilization rate between 70% and 85%. For principals, the target is lower, typically 40% to 60%, because principals spend significant time on business development and firm management. The latest Deltek Clarity study puts the median firm-wide utilization rate at about 61%, but that is a firm-wide average that includes everyone from admin to leadership.