Architect insurance is one of those topics that nobody wants to think about until they absolutely have to. But understanding your coverage (from professional liability and errors and omissions insurance to claims-made policies, tail coverage, and risk management strategies) is what separates architects who survive a claim from those who don’t. This guide breaks it all down so you can protect your practice and pass your ARE exams with confidence.

This podcast is also available on YouTube, Spotify, and Apple Podcasts.

The Reality Check: When Insurance Suddenly Matters

Early in my career, I had a renovation project in an old downtown building. Beautiful space, great client, everything going smoothly until a small electrical fire broke out during construction.

Nobody was hurt, thankfully. But there was about $20,000 in damage. Then came the finger-pointing.

The owner blamed the contractor. The contractor blamed the electrical engineer. And everyone was looking at me asking, “So… whose insurance is covering this?”

It was like a very expensive game of “Not It!” and everyone expected me, as the architect, to be the referee.

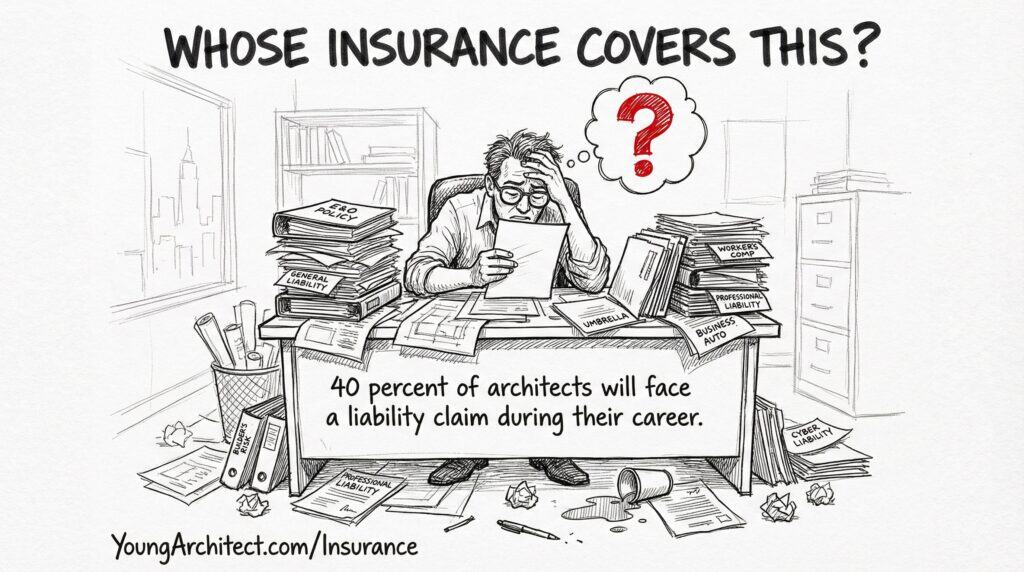

I had no idea whose insurance would cover this. They definitely didn’t teach that in architecture school.

This kind of scenario happens more often than you’d think. Industry surveys suggest approximately 40% of architects will face a liability claim during their career.

Understanding architect insurance isn’t just about protecting your practice. It’s essential knowledge for your ARE exams, especially in the Practice Management (PcM) and Project Management (PjM) divisions. Think of it like learning how to use a fire extinguisher: boring information until you really need it.

This guide will walk you through every major coverage type, what it costs, how claims actually work, and the legal terminology that shows up on both the exam and in real practice.

1. Essential Architect Insurance Types You Need

Let’s start with what you actually need to protect your practice. There are a few non-negotiables here, and a few others that depend on how your firm is structured.

Professional Liability / Errors and Omissions (E&O) Architect Insurance

Professional liability insurance (also called errors and omissions insurance or E&O insurance) is your absolute must-have. It’s like having an expensive umbrella you hope you never open, but you’ll be glad you have it when it starts pouring lawsuits.

E&O insurance protects you when someone claims you made a mistake in your professional services. Maybe your structural calculations were off, or you specified the wrong material. Even if you’re extremely careful, no set of drawings is perfect.

This is also the coverage most directly tied to the professional standard of care: the legal benchmark for what a reasonably competent architect would do under similar circumstances.

What E&O covers:

- Design errors

- Omissions in construction documents

- Failure to meet professional standards

- Negligent acts in performing professional services

What E&O does not cover:

- Intentional wrongdoing

- Contractual liability beyond your standard of care

- Faulty workmanship by contractors

Standard limits typically start at $1 million per occurrence and $2 million aggregate for small to mid-size firms. The right amount depends on your project types and risk exposure. A good rule of thumb: your per-claim limit should exceed the value of your largest project.

Worth knowing: Most E&O claims against architects don’t even involve actual errors. They’re often just allegations that get settled to avoid costly litigation.

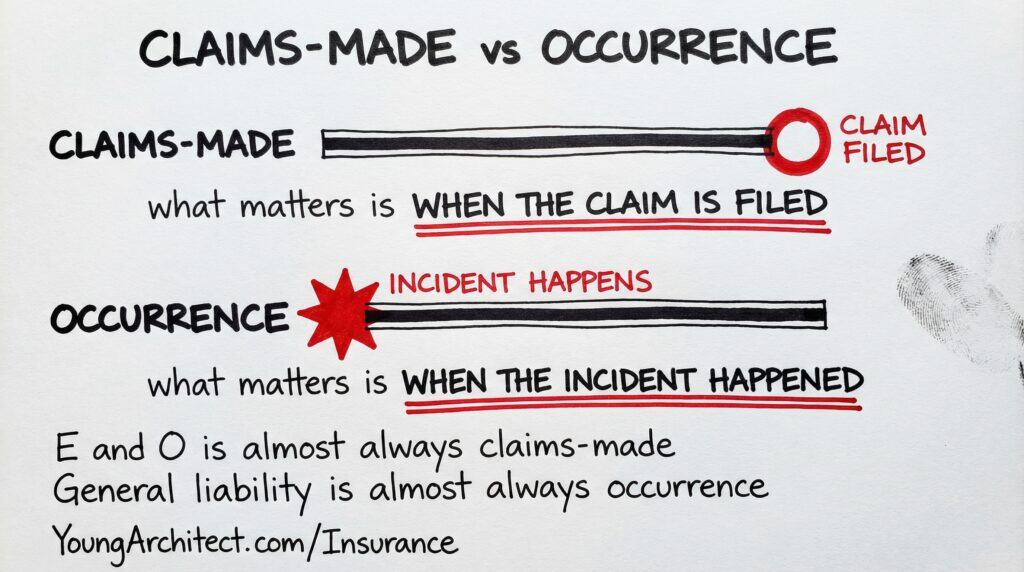

Claims-Made vs. Occurrence Policies

This distinction trips up a lot of people on the ARE, so let’s make it clear.

A claims-made policy covers claims that are filed during the active policy period, regardless of when the actual work was performed.

An occurrence policy covers incidents that happened during the policy period, regardless of when the claim is filed later.

Here’s the industry standard pairing that every PcM candidate should know:

- Professional liability (E&O) is almost always claims-made

- General liability is almost always occurrence-based

For architects, the claims-made structure means you need continuous coverage to avoid gaps. If your policy lapses (even for a short period) work performed during that gap may be unprotected if a claim comes in later. That’s where tail coverage comes in.

For more on how claims-made policies work in practice, The Hartford has a solid breakdown of claims-made vs. occurrence policies.

Tail Coverage and Extended Reporting Periods

Tail coverage (also called an extended reporting period) lets you report claims after your claims-made policy ends.

You need it when:

- You’re retiring

- You’re closing your firm

- You’re switching to a new insurance carrier

Without tail coverage, claims for work done during your active policy period could go uncovered if they’re reported after the policy expires. Typical tail coverage periods run one to three years, though unlimited options exist for retiring architects.

This isn’t a nice-to-have. It’s essential protection for work you’ve already completed.

Prior Acts Coverage

Prior acts coverage protects you when switching insurance carriers. Every claims-made policy has a retroactive date: the earliest date from which prior work is covered under the new policy.

If your new carrier’s retroactive date doesn’t go back far enough, you could have a gap in coverage for older projects. A lot of architects don’t learn about this until it’s too late.

When changing carriers, always confirm that your new policy’s retroactive date matches or predates your original coverage start date.

General Liability Insurance

While professional liability covers your design work, general liability insurance protects against everyday physical accidents.

What it covers:

- Bodily injury to third parties: a client trips over your laptop cord during a site visit

- Property damage: you accidentally knock over something valuable at a client’s office

- Personal and advertising injury: claims of libel, slander, or copyright infringement

Think of it this way: general liability covers the physical side of running a business. Professional liability covers the intellectual side of your work. You need both.

And remember: general liability is almost always an occurrence-based policy, which means incidents that happen during the policy period are covered even if the claim comes in years later.

Workers’ Compensation

Once you hire employees, workers’ compensation becomes essential. It covers your staff if they’re injured on the job, including during site visits.

Unlike professional liability and general liability (which are typically contractual requirements), workers’ compensation is a statutory requirement mandated by state law. Most states require coverage as soon as you hire your first employee. Some states have exemptions for sole proprietors or partnerships, but opting in is usually smart protection regardless.

Additional Coverage Types

Depending on your practice, you might also need:

- Business property insurance: protects office equipment and physical assets

- Cyber liability insurance: increasingly important as more work lives in the cloud

- Employment practices liability: protection against claims of discrimination or harassment

- Project-specific excess coverage: for high-value or high-risk projects

2. How Much Does Architect Insurance Cost?

This is the question everyone has but nobody asks until they’re getting their first quote. Let’s put some real numbers on it.

A safe estimate for total insurance overhead (professional liability, general liability, workers’ comp, and other standard coverages combined) is roughly 2-5% of your firm’s gross revenue.

If you’re looking at professional liability alone, the range is typically 1-3% of gross revenue for a standard firm.

Rough annual ranges by firm size:

- Solo practitioner: approximately $2,000-5,000/year for E&O

- Small firm (5-10 employees): approximately $5,000-15,000/year

- Mid-size firm: costs scale significantly based on revenue, project types, and claims history

Factors that affect your premium:

- Firm revenue

- Project types (residential work typically costs more to insure than commercial)

- Claims history

- Geographic location

- Risk management practices in place

Architect insurance is a legitimate business overhead expense. It should be factored into your architect fee structures, not absorbed as a personal cost. Most architects build it into their overhead rate when calculating fees.

The good news: there are concrete steps you can take to lower your premiums. We’ll cover those in the risk management section below.

3. Insurance Requirements for Project Participants

Understanding what coverage other parties should carry is just as important as knowing your own. It tells you who’s responsible when something goes wrong and helps you verify compliance during construction administration.

Contractor Insurance Requirements

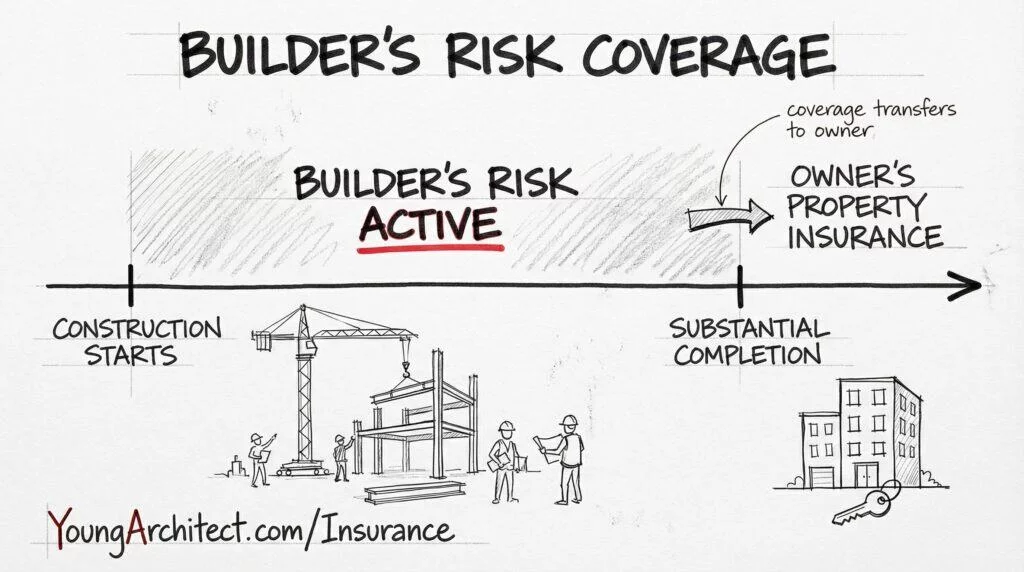

Builder’s Risk Insurance

Builder’s risk insurance is the contractor’s primary coverage during construction. It protects the building and materials while work is underway.

Builder’s risk typically covers:

- Fire damage

- Weather damage

- Theft and vandalism

- Material damage during transit

The policy period usually begins when construction starts and ends at substantial completion, when the owner’s property insurance takes over. In my electrical fire scenario from the opening, builder’s risk would have been the primary policy to handle that damage.

Contractor’s General Liability

Contractors carry general liability similar to architects, but typically with higher limits ($2-5 million) due to the physical nature of their work.

A critical component is completed operations coverage, which protects against claims arising from the contractor’s work after the project is complete. This matters because defects often don’t show up until months or years after construction ends.

Workers’ Compensation

Given the physical risks of construction, workers’ compensation is absolutely essential on job sites. As the architect administering the contract, you should verify that contractors maintain proper coverage throughout the project.

OCIP Insurance: Owner Controlled Insurance Programs

On larger projects (especially public ones) you may encounter an Owner Controlled Insurance Program (OCIP), sometimes called a wrap-up policy. These are typically reserved for large-scale institutional or public construction projects where the project size justifies the administrative complexity of a single program. The owner purchases coverage that covers most parties on the project, including the general contractor and subcontractors.

A similar structure called a Contractor Controlled Insurance Program (CCIP) puts the general contractor in the same role instead of the owner.

Pros of OCIPs:

- Streamlined coverage across all parties

- Potentially lower overall project insurance costs

- Fewer coverage gaps and disputes over which policy responds

Cons of OCIPs:

- The owner controls the coverage terms, so you have less say in policy details

- Coverage gaps can still exist for design professionals

Here’s the critical thing to know: even when enrolled in an OCIP, architects are almost always required to maintain their own separate professional liability insurance. Wrap-up policies typically cover general liability and workers’ comp. They rarely cover design errors and omissions. Never assume an OCIP replaces your E&O coverage.

Insurance requirements can differ significantly between public vs. private architecture clients, with public entities typically having more stringent requirements.

Owner Insurance Requirements

Owners typically need property insurance once a project is complete. During construction, they may need additional coverage if they’re occupying part of the building while work is ongoing.

On larger projects, owners sometimes step into the OCIP role described above, purchasing coverage for everyone involved. This can streamline the claims process significantly when incidents occur.

4. Understanding Architect Insurance Claim Scenarios

Theory is one thing. Let’s look at how insurance actually responds when something goes wrong.

Scenario 1: Design Error Claims

Imagine you’ve specified an HVAC system that proves inadequate for the building’s needs. The owner faces significant costs to upgrade the system and files a claim against your firm.

Your professional liability insurance would:

- Assign legal counsel to defend you

- Investigate whether your design actually fell below the standard of care

- Cover settlements or judgments if you’re found liable, up to your policy limits

Documentation is your best defense. Maintain records of all communications, design decisions, and client approvals. Your future self will thank you when you’re trying to remember why you specified something five years ago.

Think of documentation as your professional best friend. The more detailed, the better. Thorough documentation will save you and it’s one of the most effective risk management tools you have.

Scenario 2: Construction Phase Claims

Construction sites are inherently risky. If a structural element fails during construction, multiple parties might be involved: you, the contractor, the structural engineer, and material suppliers.

Each party’s insurer will defend their client and try to limit liability. This is where the hold harmless clauses in your contract become critical. They help establish who bears responsibility in different scenarios.

As an architect, your observation role during construction administration is a significant liability exposure. Clear documentation of site visits, field reports that distinguish between observation and supervision, and prompt communication of issues are essential practices. For more on that process, see our guide to construction submittals.

Scenario 3: Project Delivery Methods and Insurance

Different project delivery methods create different insurance needs.

- Design-Bid-Build: Responsibilities are clearly separated between design and construction, making insurance coverage more straightforward.

- Design-Build: Blurs the lines between design and construction, potentially increasing architect risk exposure. Special endorsements or project-specific policies may be necessary.

- Joint ventures: Often require dedicated insurance policies covering the joint entity, in addition to each firm’s individual coverage.

Scenario 4: Multiple Parties in a Claim

Here’s where it gets complicated. A balcony collapses on a newly completed building. The owner sues everyone: you, the contractor, the structural engineer, the material supplier.

Each party’s insurer assigns legal counsel and investigates to limit their client’s liability. As the architect, your E&O insurer will defend you and determine whether your design contributed to the failure.

This is why understanding construction claims and disputes matters before you’re in the middle of one. The time to understand the process is not when you’re already being sued.

5. Legal Terminology You Need to Know

Understanding architect insurance and the ARE exam requires knowing the following terms cold. These concepts show up in both real practice and on the PcM and PjM exams.

If you want to master this material for the exam, AIA Contracts 101 covers B101, A201, and C401 in detail, including all the insurance and indemnification clauses that appear on the ARE.

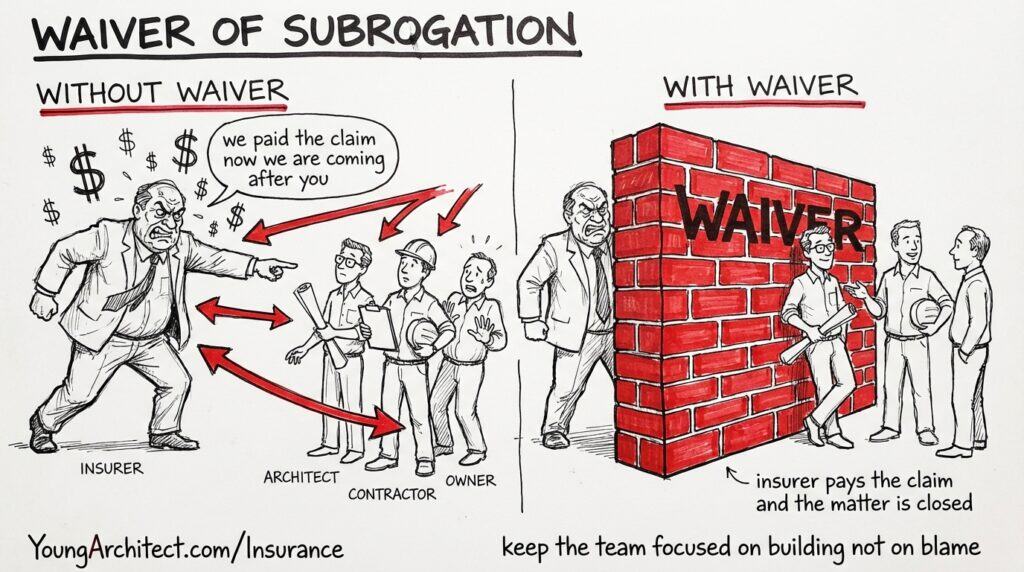

Waiver of Subrogation in Construction

Subrogation is when your insurance company pays a claim on your behalf and then pursues the responsible party to recover that money. Basically, your insurer steps into your shoes to go after whoever caused the problem.

A waiver of subrogation prevents that from happening. When both parties agree to a waiver, they’re telling their insurers: don’t go after the other team members after you pay us.

Here’s a practical example:

A subcontractor accidentally starts a fire during construction. The owner’s builder’s risk insurer pays $500,000 to cover the damage. Without a waiver of subrogation, that insurer could then turn around and sue the architect or contractor to recover the $500,000, even though the owner has already been made whole. With a waiver in place, the insurer pays the claim and the matter is closed. No one on the project team gets dragged into litigation.

This is the most common and most tested application of waiver of subrogation: property damage covered by builder’s risk or the owner’s property insurance. Waiver of subrogation clauses are standard in AIA construction contracts (see AIA A201) and exist specifically to keep project team members from fighting each other after a claim is paid.

The goal is simple: keep the team focused on building, not on blame.

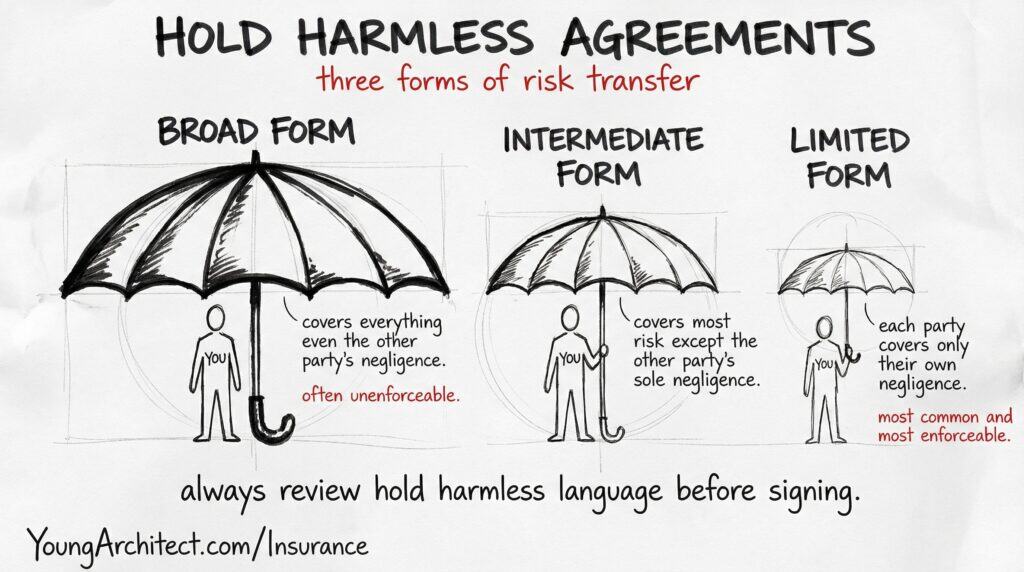

Hold Harmless Agreements and Clauses

A hold harmless agreement is a contractual provision where one party agrees not to hold another party legally responsible for claims, damages, or losses arising from specific circumstances. These are extremely common in construction contracts and subconsultant agreements.

Hold harmless clauses come in three forms:

- Broad form: One party assumes all liability, even for the other party’s negligence. Most states have anti-indemnity statutes that limit or void these.

- Intermediate form: One party assumes liability except when the other party is solely negligent. More commonly enforceable.

- Limited form: Each party is only responsible for their own negligence. This is the most common and most enforceable form.

Enforceability varies significantly by state. Many states have anti-indemnity statutes that restrict how broad these clauses can be, particularly in construction contracts. Always review hold harmless language carefully before signing.

Indemnification

Indemnification means one party agrees to compensate another for losses. These provisions are common in architectural contracts but require careful review.

Many indemnification clauses are uninsurable because they exceed what your professional liability policy actually covers. Watch for language that goes beyond your standard of care obligations.

The phrase “to the fullest extent permitted by law” is critical in indemnity clauses. Many states limit what can be legally indemnified, so this language provides a built-in cap. Without it, you could be agreeing to obligations your insurance won’t back up.

Additional Insured vs. Named Insured

These two terms sound similar but represent very different levels of coverage.

- Named insured: The policyholder. You have full coverage, full rights under the policy, and full control over claims.

- Additional insured: A party added to someone else’s policy. Coverage is limited to claims arising from the named insured’s work. You don’t control the policy and have no rights beyond that specific coverage.

In practice: architects should typically be named as additional insureds on contractor policies. Consultants should be additional insureds on the architect’s general liability policy, but not on the professional liability policy, since that coverage is specific to your design services.

For a deeper look at how consultant agreements structure these relationships, see our guide to the AIA C401 architect-consultant agreement.

Certificates of Insurance

Certificates of insurance provide evidence that coverage exists, but they have real limitations. They prove coverage existed when issued. They don’t guarantee the policy is still active or hasn’t been modified since.

Always verify certificates carefully. Check for:

- Policy types and coverage limits

- Effective and expiration dates

- Additional insured endorsements

- Waiver of subrogation provisions

Collecting a certificate at the start of a project isn’t enough. For longer projects, request updated certificates annually.

6. Architect Insurance Financial Considerations

Risk Management Strategies to Lower Your Premium

Insurance costs are significant, but you have more control over them than you might think. Many insurers offer premium discounts for firms that demonstrate strong risk management practices.

Steps that can lower your architect insurance premium:

- Implementing quality control procedures and document review systems

- Using well-crafted standard contracts (AIA forms are your friend here)

- Limiting high-risk project types, particularly residential

- Maintaining thorough project documentation

- Investing in continuing education for your staff

The AIA Trust offers a coordinated professional liability program with risk management resources specifically for architects, including a risk mitigation credit for qualifying AIA members. Learn more about professional liability options from the AIA Trust.

For a deeper framework on building a risk management program, the AIA Trust’s guide to building an effective risk management program is a solid starting point. The AIA’s risk management guide for architects is also worth bookmarking.

Long-Term Coverage Considerations

The claims-made nature of professional liability insurance creates potential coverage gaps at key career transitions. Plan ahead for these situations:

- Changing carriers: Confirm your new policy’s retroactive date covers your prior work. If not, negotiate prior acts coverage.

- Retiring or closing your firm: Purchase tail coverage (extended reporting period) to protect against claims on completed work.

- Statute of repose: Most states have a statute of repose that limits how far back claims can reach, typically 6-10 years. Your tail coverage period should at minimum cover this window.

7. Common Architect Insurance Mistakes to Avoid

Even with the right policies in place, firms still leave themselves exposed. These are the most common coverage traps architects walk into — and how to avoid them.

Inadequate Coverage Limits

Many architects underinsure to cut costs and leave themselves exposed to claims that exceed their limits. Remember the rule: your per-claim limit should exceed the value of your largest project.

If you’re taking on a $5 million project, a $1 million policy limit is a serious exposure problem.

Risky Contract Language

Watch for contractual provisions that your insurance won’t actually cover. These include:

- Guarantees of perfection or warranties beyond your standard of care

- Overly broad indemnity clauses

- Responsibility for contractor means and methods

- Language requiring you to “ensure,” “certify,” or “guarantee” outcomes

How your business entity type is structured also affects your personal liability exposure. An LLC or LLP creates a liability shield that a sole proprietorship doesn’t. Your entity choice and your insurance coverage work together.

Documentation Failures

Poor documentation is the most common reason architects lose claims they should win. Maintain thorough records of:

- Client communications and written approvals

- Design decisions and the reasoning behind them

- Field observations and site visit reports

- Project meeting minutes

- Change orders and their justifications

Understanding the relationship between drawings vs. specifications is also critical here. Conflicts between these contract documents are a common source of claims, and clear documentation of intent can protect you when disputes arise.

Coverage Gaps

Common coverage gaps that architects miss:

- Lapsed policies during firm transitions

- Inadequate prior acts coverage when switching carriers

- Missing endorsements for specific service types

- International project exclusions

- Joint venture exposure not covered by individual firm policies

Notification Failures

Most policies require prompt reporting of potential claims, not just actual claims. If you become aware of a situation that might become a claim, notify your insurer immediately.

Failing to notify your insurer of potential issues can void your coverage entirely, even if the formal claim comes in later. When in doubt, report it. That’s what your insurer is there for.

Understanding how construction claims and disputes actually play out will help you recognize the warning signs early and report them before they escalate.

Frequently Asked Questions: Architect Insurance

How much does architect insurance cost?

Professional liability insurance alone typically runs 1-3% of your firm’s gross revenue. Total insurance overhead (E&O, general liability, workers’ comp) is closer to 2-5%. For solo practitioners, E&O often costs $2,000-5,000 per year. Small firms with 5-10 employees might pay $5,000-15,000 annually. Project type, claims history, and location all affect your rate. See our guide to architect fee structures for how to factor insurance into your overhead rate.

What is tail coverage in insurance?

Tail coverage (also called an extended reporting period) lets you report claims after your claims-made policy expires. Since most architect E&O policies are claims-made, you need tail coverage when retiring, closing your firm, or switching carriers. Without it, claims for completed work could go uncovered if they’re reported after your policy ends. Tail coverage periods typically run one to three years, though unlimited options exist.

What is the difference between claims-made and occurrence policies?

Claims-made policies cover claims filed during the active policy period, regardless of when the work was performed. Occurrence policies cover incidents that happened during the policy period, regardless of when the claim is filed. Professional liability is almost always claims-made. General liability is almost always occurrence-based. This pairing is a common topic on the PcM exam. Read more about the professional standard of care to understand how claims are evaluated.

What is a waiver of subrogation in construction?

A waiver of subrogation prevents an insurance company from pursuing another project team member to recover money after paying a claim. Without it, an insurer could pay a fire damage claim and then sue the architect or contractor to get their money back, creating conflict on the project team. Waiver of subrogation clauses are standard in AIA construction contracts (A201) and protect everyone on the team from post-claim litigation between insurers.

Do architects need errors and omissions insurance?

Yes. Errors and omissions (E&O) insurance is the most important coverage an architect carries. It protects against claims of design errors, document omissions, negligence, and failure to meet the professional standard of care. Even if you never make a mistake, you can still face allegations that require legal defense. Most clients and project contracts require architects to carry E&O coverage before work begins.

Protect Your Practice and Pass Your Exams

Architect insurance might not be the most exciting topic in the world, but it’s your safety net when things go sideways. Think of it like the guardrails on a mountain road: you don’t appreciate them until you really need them.

Quick recap of what every architect needs to know:

- Architects need professional liability (E&O) and general liability insurance at minimum

- Professional liability is almost always claims-made; general liability is almost always occurrence-based

- You need tail coverage when retiring, closing, or switching carriers

- Waiver of subrogation keeps project team members from fighting each other after a claim

- Contractors need builder’s risk, general liability, and workers’ compensation

- Even in an OCIP, architects almost always need their own separate professional liability coverage

- Documentation is your best defense in any claim

Insurance, risk management, and contract law are core topics on the Practice Management and Project Management exams. If you want structured help working through this material, PcM 101 covers firm-level business operations in depth, and PjM 101 covers contract structure and consultant coordination from the project level.

For a deep dive into AIA contracts (including all the insurance and indemnification clauses in B101, A201, and C401) AIA Contracts 101 breaks it all down.

Ready to get licensed? Join ARE Boot Camp for structured coaching, accountability, and a clear roadmap through all six exams. Or get access to all our self-paced study materials with the ARE 101 Membership.